Five years after it implemented the Herschell Committee recommendations in 1893, the Government of India made fresh proposals. The British Government, in turn, appointed the Fowler Committee in 1898 to examine these proposals.

In 1893, as endorsed by the Herschell Committee, and approved by the British Government, the Indian Government discontinued silver coinage. The intention was to eventually introduce a gold standard, the most important step in ensuring an exchange rate of 1s. 4d. This was not achieved for nearly five years. Therefore, the Government of India submitted fresh proposals to the Secretary of State for India to hasten the process. Some of these were drastic. These included the sale of bullion worth £ 6 million. There was also to be a sterling loan issued to make good the loss.

The Fowler Committee

On 29 April 1898, the Secretary of State referred the matter to a large Committee. Sir Henry H. Fowler headed the ‘The Committee Appointed to Inquire into the Indian Currency’. The Committee became known as the Fowler Committee, and its report, the Fowler Report. Lord George Hamilton, the Secretary of State for India, in his letter of 28 April 1898, laid down the objectives:

“It will be the duty of the Committee to deliberate and report to me upon these proposals and upon any other matter which they may regard as relevant thereto, including the monetary system now in force in India, and the probable effect of any proposed changes upon the internal trade and taxation of that country; and to submit any modifications of the proposals of the Indian Government, or any suggestions of their own, which they may think advisable for the establishment of a satisfactory system of currency in India, and for securing, as far as is practicable, a stable exchange between that country and the United Kingdom.”

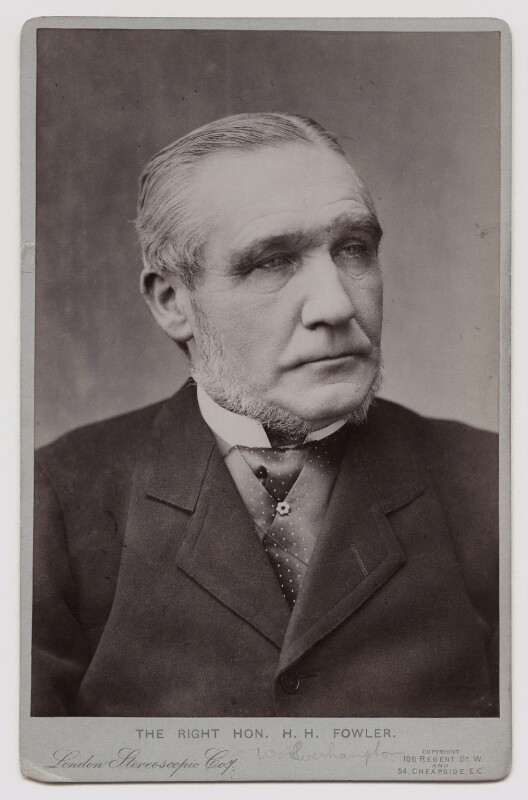

Henry Fowler

Henry Hartley Fowler (1830-1911), the future First Viscount of Wolverhampton, was himself the Secretary of State for India during 1894-95. He was also a member of the Privy Council, and Secretary to the Treasury. He remained in contention for long as a future Prime Minister. But, bad health came in the way. A Methodist in upbringing, he approached complex issues with equanimity studying different aspects of the problem. So much so, politicians of all hues sought his views. As Edith Fowler later wrote in her biography of her father, it was common to ask, “What does Fowler say?”

The Fowler Committee members

A Committee’s composition often indicates its importance and sometimes even the desired outcome. The other members of the Fowler Committee were Balfour of Burleigh, John Muir, Francis Mowatt, David Barbour, C.H.T. Crosthwaite, Alfred Dent, F.C. Le Marchant, E.A. Hambro, W.H. Holland, and Robert Campbell. Robert Chalmers was the Secretary. Some of them we will encounter again as we go along with the history of currency and central banking in India.

Lord Balfour

Alexander Bruce, the 6th Lord Balfour of Burleigh, was a Scottish Unionist politician, banker and statesman, who took a leading part in the affairs of the Church of Scotland. He was then a Secretary for Scotland and would become a long standing Governor of the Bank of Scotland (a commercial bank) from 1904 to 1921.

Sir John Muir

Sir John Muir was a Scottish businessman who started work with James Finlay & Co. He later set up Finlay Muir & Co. in India with business interests in cotton, tea, rubber, and jute. At its peak, it was the world’s leading growers and packers of tea. By the time of the Fowler Committee’s work, the company controlled around 270,000 acres of plantations, more than a quarter of which was in tea. It was one of the largest companies worldwide, with around 90,000 employees, of which 70,000 were in India.

Sir Francis Mowatt

Sir Francis Mowatt, a civil servant, was then the Permanent Secretary of the Treasury, a position he would hold for almost a decade from 1894. His lesser known claim to fame was training Winston Churchill at the Board of Trade as a free trader. This prompted, in 1904, the first of Churchill’s two famous crossings of the floor, from the Conservative to the Liberal Party. The second came in 1924, soon after which he became the Chancellor of the Exchequer. In this capacity, Churchill reintroduced the gold standard in England. He was also instrumental in appointing the Hilton Young Commission which we will discuss in due course.

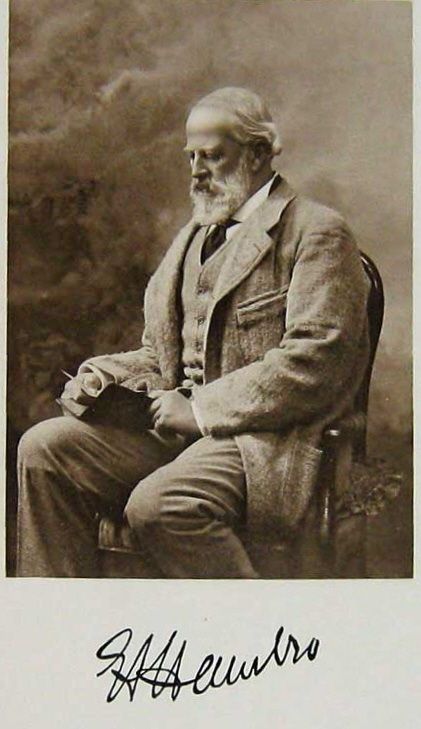

Sir Everard Hambro

Sir Everard Hambro came from a banking family, starting his career with the Hambro Bank. He was at the time a director of the Bank of England. He served on the Bank’s Court for nearly a half century from 1879 till his death in 1925.

Sir David Barbour

We had encountered Sir David Barbour in the last part on the Herschell Committee. As the Finance Member in the Viceroy’s Executive Council, he had drafted the earlier proposals for moving towards a gold standard.

Sir Charles Crosthwaite

Sir Charles Crosthwaite was a civil servant with the Bengal cadre. He had served as Chief Commissioner of Burma from 1887 to 1890. He would later, in 1912, publish The Pacification of Burma, an account of the work done to bring about peace in Burma after its annexation under Lord Dalhousie in 1852.

Other members

Sir Alfred Dent was a British merchant who had founded the British North Borneo Company. This company administered North Borneo till 1946, much like the East India Company in India till 1857.

F.C. Le Marchant was a member of the Council of the Secretary of State for India.

Sir William H. Holland was a British industrialist and Liberal politician.

The identity and background of Robert Campbell were not ascertainable. He was probably a banker or a partner in a Calcutta-based firm. Generations of Campbells worked in India, in the East India Company, in the Indian Civil Service, and in industry and finance.

Sir Robert Chalmers

The star of the Committee, in this author’s view, neither the Chairman nor a member, but its Secretary, Sir Robert Chalmers. There was criticism that the group did not have much experience in Indian currency. Counter evidence comes, in addition to Sir David Barbour and Sir Everard Hambro, from Sir Chalmers.

A British civil servant, and a Pali and Buddhist scholar, Chalmers translated over 2000 texts on Buddhism. Apart from articles and books on Pali and Buddhism, he authored, in 1893, A History of Currency in the British Colonies, a standard reference on the subject. This alone makes up for any deficiency in the experience of others. Among those associated with the Fowler Committee, Chalmers alone became a member of the Chamberlain Commission and the Babington-Smith Committee that followed in 1913 and 1919. He later served as Governor of Ceylon.

In its report, the Committee appreciated Chalmers’ work: “We desire to express our high appreciation of the assistance which Mr. Chalmers has rendered to us throughout the whole course of this inquiry. We feel it to be our duty to recognise in the strongest terms the knowledge, ability, courtesy, and industry which he has displayed and which have greatly facilitated our labours.”

The 1893 proposals

The Government of India had, in a telegram of 22 January 1893, further elaborated its earlier proposals which formed the basis for appointing the Herschell Committee. It stated as follows:

“Our proposal is that we shall take power to issue a notification declaring that English gold coins shall be legal tender in India at a rate of not less than 13 1/3 rupees for one sovereign [i.e., 18d. per rupee]… An interval of time, of which the length cannot be determined beforehand, should, we think, elapse between the mints being closed and any attempt being made to coin gold in India. The power to admit sovereigns as legal tender might be of use as a measure ad interim, but it need not be put into force except in case of necessity.”

That period from the date of closing the mints for silver coinage was five years. Even after five years, stability in the exchange rate was beyond reach. That was the rationale for appointing the Fowler Committee.

The Fowler Committee – Evidence

The Fowler Committee held 43 meetings and examined 49 witnesses. The witnesses included Prof. Alfred Marshall, the first Professor of Political Economy, and the best known economist of his time, from the Cambridge University. Then there was Sir Robert Giffen of Giffen goods fame. There were two from the Rothschild family. Lord Aldenham, former Governor, Bank of England, was another significant witness. Another key witness, examined over two full days, was James McKay, later Lord Inchcape, who headed the Inchcape Committee on Indian Railways in the early 1920. We discussed this Committee in an earlier post on Sir Purshotamdas Thakurdas (see here).

The other witnesses were administrators, businessmen, traders and bullion dealers, bankers, etc. Most had long years of experience living in India or dealing with India, or having a more than casual interest in the exchange rate of Indian currency. Some of the witnesses were members of the earlier Herschell Committee or had given evidence before it.

Indian witnesses

There were only two Indians among the witnesses. One was Romesh Chunder Dutt, civil servant and economic historian. One among the first Indians to join the Indian Civil Service, he had retired the previous year. He had not yet written his classic two volume economic history of India. But, he was back in London to teach Indian history at the University College. Dutt would later become Dewan of the Baroda State with which he had close links.

The second was Mr. Merwanjee Rustomjee, a broker dealing in exchange, finance, bullion, and government securities. He was representing the Bombay Native Shares, Stock, and Exchange Brokers Association, now known as the Bombay Stock Exchange.

The Fowler Committee Report

The Fowler Report is a short report. Its 71 paragraphs is only 21 pages long in one print version. There are another six pages of comments by members, individually or in groups. The brevity was in part aided by the wealth of detail already available in the Herschell Committee Report. The Herschell Report had left unsaid the modalities for implementing a gold standard that it had recommended. This was what the Fowler Report proceeded to do.

Fowler Committee Recommendations

The Fowler Committee recommended the continuance of the Indian Government proposals made in 1892 and implemented in 1893. It concurred with the Government of India in their decision not to revert to the silver standard. It further recommended establishing a gold currency, making the sovereign legal tender. Also recommended was opening the Indian mints to unrestricted coinage of gold, receiving gold and reissuing them as coins. The exchange rate for gold was to be fixed at 15 rupees to the sovereign or 1s. 4d. per rupee (one shilling and four pence), as originally contemplated in 1893.

The Exchange Rate

The Committee did not recommend any change in the relation between the sovereign and the rupee: “Theexperience gained since the mints were closed in 1893, and particularly that of the last eighteen months, appears to us to justify the anticipation that the existing rate of 1s. 4d. will, with possible temporary fluctuations, due to the course of trade, be maintained in the future.”

The exchange rate was a bone of contention right up to the Hilton Young Commission in 1925-26.

Fowler Committee defence

The Fowler Committee tried to deemphasise its importance stating that there was no net gain to the country by a depreciation of the currency:

“In our opinion a rise in prices which expresses only the depreciation of the currency is no gain to the community as a whole, and, although the fixing of a lower denomination in sterling for the rupee might for a time give some advantage to producers and induce for a limited period a larger importation of gold than would otherwise take place, this would be at the expense of every holder of a rupee, or debt or security for a fixed amount of rupees; and the taxpayer would again be compelled to provide a larger amount of currency to meet the sterling requirements of the State. It is not by such an expedient as the writing-down of the rupee in sterling that a permanent stimulus can be given to production or to the importation of the standard metal.

… We see no sufficient reason for altering the existing relations of prices and the essential conditions of contracts expressed in Indian currency, or for reversing the course of exchange and returning to some basis of value which may have prevailed during the interval between the fall and partial recovery in the sterling value of the rupee, and which does not possess elements of permanent stability in a higher degree than the present rate. We are, therefore, of opinion that the permanent rate should be that which has been adopted as the provisional rate in the past, and which is also the market rate of to-day, viz., 1s. 4d. for the rupee.”

Gold standard

The Committee was “impressed by the evidence of Lord Rothschild, Sir John Lubbock, Sir Samuel Montagu, and others, that any system without a visible gold currency would be looked upon with distrust.” It, therefore, recognised that the practical alternative to silver mono-metallism was a gold standard, with gold as the measure of value, either with a gold currency or a gold reserve. It further concluded “that steps should be taken to avoid all possibility of doubt as to the determination not to revert to a silver standard, but to proceed with measures for the effective establishment of a gold standard.”

By way of conclusion, the Committee recorded that “the effective establishment of a gold standard is of paramount importance to the material interests of India. Not only will stability of exchange with the great commercial countries of the world tend to promote her existing trade, but also there is every reason to anticipate that, with the growth of confidence in a stable exchange, capital will be encouraged to flow freely into India for the further development of her great natural resources. For the speedy attainment of this object, it is eminently desirable that the Government of India, with whom it will rest to decide when successive steps should be taken, should husband the resources at their command, exercise a resolute economy, and restrict the growth of their gold obligations.”

Holland’s note of dissent

Why not postpone

Sir William Holland did not want to fix a permanent rate at once, but preferred to leave it to be decided in the light of further experience. As he elaborated,

“Since the Committee was appointed, the condition of the money market in India has so greatly improved that the immediate settlement of the currency question has, in my opinion, become less urgent than it was in the spring of 1898…

“It may be that further experience will show the balance of advantage to be with a lower exchange than 1s. 4d.; or, on the contrary, circumstances might conceivably arise (e.g., silver legislation in the United States) which would necessitate a higher rate. In view of these possibilities, and of the fact that the existing monetary conditions of India are not, in my judgment, producing any serious evils, I am of opinion that no action should be taken at the present time, in the direction of finally settling the rate between the sovereign and the rupee; but that the question should be left to be decided in the fuller light which would be afforded by further experience.”

Holland on gold as legal tender

Holland had this also to add on having gold as legal tender:

“Under existing conditions, gold is not – in form – a legal tender in India; yet, for all practical purposes, the sovereign is now a legal tender for 15 rupees, because the holder of a sovereign can obtain for it 15 rupees at the Government Treasury, and these 15 rupees, is therefore only a change in form and not in substance, and will neither strengthen exchange, nor be likely to lead to a greater import of gold into India.”

The majority, however, felt that the advantages of not taking action was “more than counterbalanced by the importance of removing doubts as to the future policy of the Government of India, and giving increased confidence to those who are engaged in commercial and financial business in connection with the Indian Empire.”

Note by Muir and Campbell

Muir and Campbell argued for a rate of 1s. 3d. instead of 1s. 4d as it will be more favourable to Indian exports. They wrote as follows:

“Going back to 1893, the conditions then prevailing clearly pointed to 1s. 3d. as the ratio which should have been adopted then; and we can see nothing in subsequent experience to justify the belief that 1s. 4d. is the more suitable ratio now. On the contrary, we consider 1s. 4d. an extreme ratio, which imposes too severe a tax on production, and is calculated to injure the trade balance necessary for India’s solvency, and that the corresponding ratio, of Rs. 15 per sovereign, by putting too low a value on gold, will tend to prevent its going into or remaining in circulation, and thereby endanger the success of the gold standard.”

They added that “We believe 1s. 3d., or Rs. 16 per sovereign, to be a ratio which would not be injurious to India’s interests, and under which she would be able to acquire by trade influences the gold necessary to make the gold standard effective.”

According to them, they were not “advocating a depreciated currency.” Instead, they felt that India was “a long way from the point at which the term depreciation would be appropriate; – the rupee at 1s. 4d. is, on the contrary, immensely appreciated, and in urging a change to 1s. 3d. we are only seeking to correct what we consider to be an excessive, arbitrary enhancement.”

The majority’s counter

In addition to its arguments earlier (see under exchange rate), the majority opinion countered this argument as follows:

The gainers and losers

“It is argued that the rate of 1s. 3d. will be more favourable to the Indian export

trade than 1s. 4d.; but we have already expressed the opinion that any advantage to the export trade that is gained in this way, is gained at the expense of other members of the community, and is only temporary. If the rate is to be fixed at 1s. 3d. in order to benefit the Indian exporters and the Indian producer of articles of export, the same argument would justify a further reduction to 1s. 2d., and so on, without any limit which we have been able to discover.

…Nor do we think there are any good grounds for holding that the gold standard cannot be established in India at ls. 4d., while it can be established at 1s. 3d. If it is impossible at 1s. 4d., it will be impossible at 1s. 3d.; and we have already dealt in paragraph 66 with the question of the temporary loss and gain to individuals and classes of the community caused by a lowering of the existing rate of exchange.”

We would add that, if the exchange were now lowered from 1s. 4d. to 1s. 3d., the

classes of the community who would gain are those who have already gained through the fall from 2s. to 1s. 4d., and the classes who would lose are those who have already lost through that fall. Stronger reasons than appear to us to exist would he needed to justify a measure which would have the effect, of adding to the gains of the former classes and intensifying the losses of the latter.”

The appropriate rate

“It is said that the conditions prevailing in 1893 show that 1s. 3d. … should have been adopted at that time. We do not accept this … conditions have changed since 1893. The rate of 1s. 3d. may have prevailed shortly before the mints were closed, but the rate …was a fluctuating rate. If the mints had been closed some years earlier, and the market rate had been adopted, the permanent rate would have been considerably higher than 1s. 4d.; if they had been closed some years later …. the permanent rate would have been lower than 1s. 3d. …between the rate of to-day and that determined by the bullion value of the rupee, there is none which can be described as natural or normal; and we can find no good reason for making the permanent rate depend upon the accident of the date on which the Indian mints were closed ….”

Comment on Herschell Committee

The majority added as follows: “It is true that Lord Herschell’s Committee remarked that “to close the mints for the purpose of raising the value of the rupee is open to much more serious objection than to do so for the purpose of preventing a further fall;” but an undue stress is laid on these words when they are used as an argument against permanently adopting a rate of ls. 4d, since that Committee actually adopted a provisional rate of 1s. 4d. and expressly said that circumstances might arise rendering it proper, and even necessary, to raise the rate.

Further, according to the majority, “… experience gained since the mints were closed in 1893, and particularly that of the last eighteen months, appears to us to justify the anticipation that the existing rate of 1s. 4d., will, with possible temporary fluctuations, due to the course of trade, be maintained in the future.” It therefore did not recommend any change in the existing relation of the rupee to the sovereign.

Campbell, Holland and Muir

Campbell, Holland and Muir, were “opposed to sterling borrowing, whether for the establishment or the maintenance of a gold standard. Borrowing to support the standard once resorted to, it would be impossible to know when to stop, and the only safe course is not to begin. It is on trade support that the maintenance of the gold standard must in the long run depend, and any saving of delay through borrowing would not be worth the risk of finding, after having incurred a load of sterling debt with its consequent addition to the home charges, that an impracticable scheme had been pursued which when left to its own merits would break down.”

Hambro calls for a central bank

The relevance of the Fowler Committee went beyond the currency question. One suggestion that the government took forward forward for some time, came from a separate note by Sir Everard Hambro. As noted earlier, he was a Director on the Court of the Bank of England. Through this note, he called for establishing an institution along the lines of the Bank of England or the Bank of France, without calling it a central bank.

This was probably the first call for a central bank after 1871. At that time, the government closed the matter on the grounds that sufficient number of qualified persons were not available to be on its Board. The Secretary of State took forward the matter through protracted correspondence with the Government of India. The efforts over two years to amalgamate the Presidency Banks as a first step towards a central bank proved infructuous.

We cover Hambro’s proposal in detail in another post.

The Fowler Committee Implementation

The first recommendation

The effective implementation of a gold standard in India was the main objective before the Fowler Committee. The other recommendations were incidental. The Committee, as mentioned earlier, had decided against reopening the mints, and in favour of fixing the rupee at 1s. 4d. The Secretary of State and the Government of India accepted these recommendations in July 1899. In 1899, the Government passed an Act making British gold coins, the sovereign and half sovereign, legal tender in India at the rate of fifteen rupees to the £, and authorising the issue of notes in exchange. The government was to redeem these notes on demand with rupees, or gold. For this purpose, the law required it to maintain a Paper Currency Reserve. This gave effect to the first recommendation of the Committee.

This was the only provision fixing the rupee rate at 1s. 4d. It prevented the rupee from rising above 1s. 4d. But it did not prevent the rupee from falling below 1s. 4d. It would have been a dead letter if it became cheaper to give 15 rupees in settlement of a debt than one sovereign. But, as the Chamberlain Commission noted in 1914, in 1898 the exchange value of the rupee touched 1s. 4d. for the first time since the closing of the mints to silver. Except for one temporary fallfor a brief period during the crisis of 1907-08, it remained fixed at 1s. 4d. ever since.

The second recommendation

The government also took steps for implementing the second recommendation, viz., opening of a mint for gold coinage. The government dropped the scheme in 1902 after nearing completion. It revived the scheme only about a decade later. The steps taken during the initial years shaped public sentiment as to the government intention to maintain the gold standard.

Gold Standard and Paper Currency Reserve

The third recommendation required segregating profits from rupee coinage as a special reserve in gold. This later became known as the Gold Standard Reserve.

The 1893 Act provided for accepting gold at the mints and Paper Currency Offices at 15 rupees per £. Another Act in 1898 authorised further issue at the same rate of notes in India against gold deposited in London. The Bank of England earmarked this as part of the Paper Currency Reserve. This Act was at first intended to be temporary. Its effect was to facilitate Government remittances to London,and to add to the gold resources of India. It also gave elasticity to the currency, allowing issue of rupees or notes in India against gold tendered in London. This issue of currency against gold in London added to the drain on the rupee reserves of the Indian Government.

Pushing gold coins

By middle of January 1900, the stock of gold in the Paper Currency Reserve in India had reached 5,000,000l. Though gold coins were legal tender, the public continued to demand rupees, and the Government considered resuming rupee coinage. Considering this drain, the government implemented the Fowler Committee recommendation to actively promote sovereigns as a medium of circulation. It asked its Currency Offices to offer sovereigns to presenters of notes, giving rupees to anyone who refused sovereigns. It also used the Post Offices and other government institutions to press sovereigns on the public. The results were unsatisfactory.

Many of the gold coins returned to the Government. It became impossible to convert currency notes intorupees not only inCawnpore (Kanpur) and other Provinces, but also in Calcutta. In Cawnpore, notes were circulating at a discount of up to 7/16th per cent. With this, the paper currency was in danger of loss of public confidence. At the same time, the sovereigns also started circulating at a discount of up to 4 annas. Famine conditions and the inadequacy of supplies of rupee coins made the condition more stringent.

Resuming rupee coinage

In the above background, the government resumed rupee coinage in 1900. The Act provisions of 1898 were continued for another two years to facilitate recourse to the London silver market. A new provision authorised using the gold in the Paper Currency Chest in London for purchasing silver for coinage. The silver so purchased were to form part of the Reserve against notes in circulation until they were minted. These provisions became permanent with an Act of 1902.

With increasing coinage of rupees, from 1900, the Government stopped forcing gold coins into circulation. The other subsequent developments which eventually led to the appointment of the Chamberlain Commission in 1913 is discussed in the next part.

Edith Fowler on the Fowler Committee

As Edith Fowler summed up in her biography of her father, “… curiously enough, it was not until after he had ceased to be Secretary of State that his chief work for Indian finance was undertaken and carried through. No one, who was not concerned with the Government of India before the adoption of a gold standard for that country, can have a conception of the boon which was conferred upon the Indian taxpayers, and on the Government which represented them, by the reform which resulted from the labours of Mr. Fowler’s Committee on the Indian currency.”

But, she does not forget to mention the ground work. “The ground had been prepared by Lord Herschell’s Committee, which sat in 1892-93, and by the closing of the Indian Mints in 1893.”

She concluded with satisfaction and pride, as follows: “But it remained for the large and important Committee, which sat five years later, presided over by Sir Henry Fowler, to complete the work of reform, and to elaborate the system which has since been introduced and has worked with perfect smoothness and success. Its success is, in fact, so great as to exceed its own greatness; and it is now difficult to recall to memory a state of things under which a fall of a penny in the gold value of silver was hardly less an object of dread to the Government of India than a war, a pestilence, or a famine. With this great and beneficent change Sir Henry Fowler’s name must always be associated.”

© G. Sreekumar 2021.

For periodical updates on all my blog posts, subscribe for free at the link below:

https://gsreekumar.substack.com/

![]()