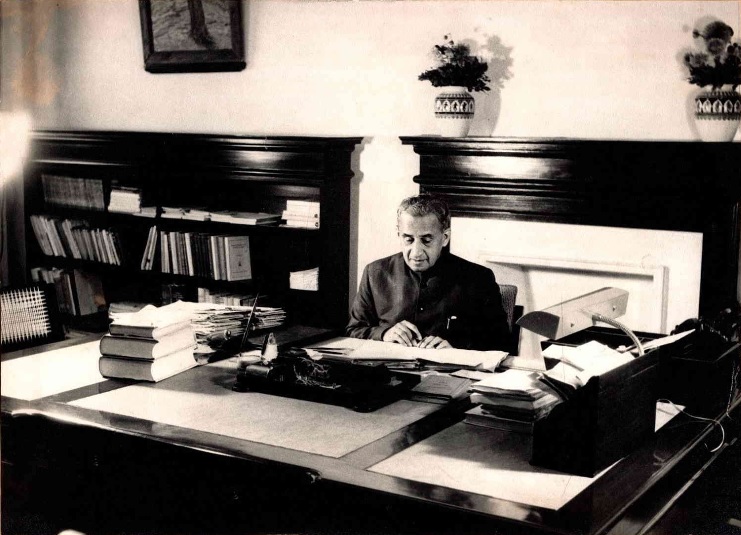

CD Deshmukh as Finance Minister at his No 1 Willingdon Crescent residence

In an earlier post on CD Deshmukh, I drew on his life and career in the context of his abiding interest in botany and of horticulture (see here). Here, I describe in greater detail, his professional career, almost devoid of personal references. A much shorter version, about one fifth in length, appeared in an online encyclopaedia of Indian economists (see here). Continue reading “The many careers of CD Deshmukh”

That wretched woman with the infant in her arms, round whose meagre form the remnant of her own scanty shawl is carefully wrapped, has been attempting to sing some popular ballad, in the hope of wringing a few pence from the compassionate passer-by.

Charles Dickens, Sketches by Boz

“Cooperation has failed, but cooperation must succeed,” is an oft-quoted extract from the 1954 report of the All India Rural Credit Survey Committee (AIRCSC). Sir Benegal Rama Rau, the fourth Governor, Reserve Bank of India, appointed the Committee. No other financial sector was the subject of scrutiny by as many committees as Indian cooperation. The quote is believed to be the contribution of Burra Venkatappaiah, of the Indian Civil Service. Venkatappaiah was then the Reserve Bank of India’s first Executive Director, and a member of the AIRCSC. He later became Deputy Governor, and the fourth Chairman of the State Bank of India. Thereafter he chaired the All India Rural Credit Review Committee which reported in 1969. I have a separate post on Venkatappaiah coming up, but my focus here is on Indian cooperation. Continue reading “Indian Cooperation: Finding Raiffeisens”

In the history of Indian currency and central banking, the Fowler Committee occupies an important position. But, its relevance went beyond the currency question. One suggestion that emanated from its report was Sir Everard Hambro’s central bank proposal. Hambro suggested establishing a state bank along the lines of the Bank of England and the Bank of France. Hambro’s central bank proposal is contained in a brief note attached to the Fowler Report. It provided the rationale for the proposal. The suggestion went back and forth between Calcutta and London before it was dropped after objections from different quarters. Continue reading “Sir Everard Hambro’s central bank proposal”

The Case of the Reserve Bank of India Circular on Opening Current Account

An oft cited paper in the literature on regulation goes by the title “Gentle Nudge vs. Hard Shove”. The regulatory dilemma is exemplified by the recent case of the Reserve Bank circular on opening of current accounts. Years of “gentle nudges” which did not result in banks complying with instructions regarding credit discipline seem to have resulted in “hard shoves” involving more hands-on regulation.

Some bank borrowers have taken the legal course demanding quashing of the Reserve Bank of India circular dated 6 August 2020 on opening current accounts by banks. The Bank has since further extended the last date for compliance to 31 October 2021. Continue reading “Opening current accounts in banks”

Sir Purshotamdas Thakurdas next made a major contribution to the work of the Indian Retrenchment Committee. The implementation of the Acworth Committee recommendations, including greater investment for railway expansion and a separate railway budget, increased government expenses substantially. The government feared that it might not be able to meet these rising expenses. Following this, the government responded by cutting expenses even by laying off people wherever possible. To find the means of doing this, it appointed the Indian Retrenchment Committee, which functioned during 1922-23. Continue reading “Purshotamdas Thakurdas, Part 3”

Purshotamdas Thakurdas, the young crusader, Sir PT or PT to friends, and as “King of Cotton” among other epithets, had a formidable reputation for his honesty, integrity, and fierce independence. He retained these characteristics while serving on up to seventy bodies. These included the Round Table Conferences, legislative councils and assemblies, committees and commissions, and trusts and boards. He served in these as trustee, director, commissioner or chairman. Moreover, PT was an untiring crusader for various public causes from a young age, including famine relief. He was also the fourth longest-serving director on the Central Board of the Reserve Bank of India. The next month, July 2021, denotes the 60th year of the passing away of Sir PT. This is the first in a series of posts covering the life and work of Sir PT. Continue reading “Purshotamdas Thakurdas as the young crusader”

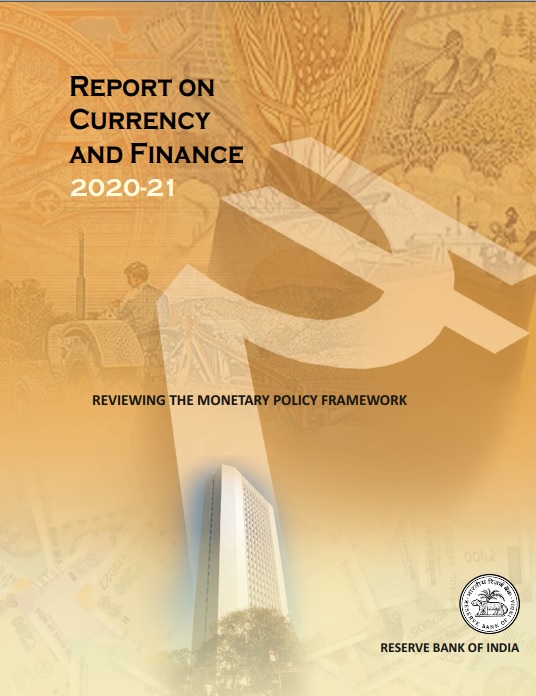

The latest issue of the Report on Currency and Finance

The Reserve Bank of India released its new Report on Currency and Finance (RCF) in February this year. This comes nearly a decade after the previous issue. The RCF is a non-statutory report, unlike the Annual Report and Report on Trend and Progress of Banking in India (RTP). The former is published under the Reserve Bank of India Act, 1934. The RTP is published under the Banking Regulation Act, 1949. The 2021 RCF is significant in three ways. It is the centenary of the first consolidated report of the Controller of the Currency, which became the RCF. For the first time, it is a discussion paper on a specific issue. It is also the first issue of RCF with a foreword signed by the Governor, Reserve Bank of India. The RCF has had a chequered history, which is worth recounting. Continue reading “The Report on Currency and Finance”

This is a post on my two brief meetings with KRK Menon, the first Finance Secretary. But, let me first start with a brief on the son. A person of Indian origin heading a global MNC no longer makes waves. Nevertheless, it is still surprising that the passing away of Bhaskar Menon in March this year, aged 86, went largely unnoticed in India, barring a few odd write-ups and mentions. Continue reading “KRK Menon, First Finance Secretary”

This post is a longer version of my article on James Wilson, the first Finance Member of the Viceroy’s Executive Council, which was published in Business Standard dated 21 January 2021. Please see the link here. Wilson was also the Founder of The Economist, and the Standard Chartered Bank. He presented the first Indian budget in 1860, and introduced income tax in the country. He also laid the foundations for introducing government paper currency in India the Indian Police, and the Office of the Comptroller and Auditor General, among other things. Continue reading “Hawick to Hawick: Life of James Wilson”